Breaking the group – capital reduction demergers

At HMT LLP, we are advising on an increasing number of corporate demergers, whereby corporate groups are split and held separately by the original shareholders.

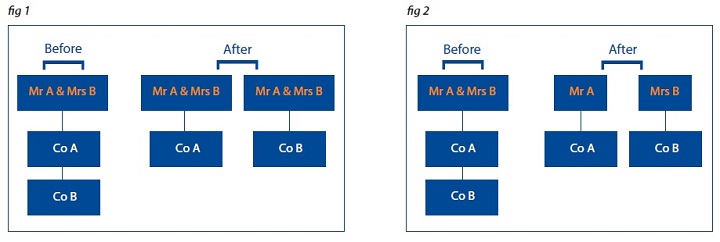

The shareholders can remain the same in both demerged groups (Fig 1), or the shareholder group can be split (Fig 2).

We have recently seen demergers used to achieve a range of business and tax objectives including:

- The shareholders want to take distinct parts of the business in different directions under separate ownership;

- The group has evolved with conflicting business streams creating customer confusion, so the shareholders move them into separate groups;

- The shareholders want to sell of part of the group and obtain Entrepreneur’s Relief (ER) by selling the shares of the exiting company directly;

- After the founder’s death, a group is owned by the extended family who wish to split the assets between two family groups so each family can protect its own wealth and pursue its own business strategy;

- A shareholder wishes to extract a property from his company before the disposal of the trading company.

There are many tax considerations both for the shareholders and the companies involved in the demerger. An incorrectly structured demerger can be an extremely expensive tax event. However, it is possible with careful planning to demerge a group with nil or with manageable tax costs.

There are three main ways a demerger can be achieved tax efficiently: a Statutory or Exempt Demerger, a Liquidation Demerger or a Capital Reduction Demerger.

The Statutory or Exempt Demerger was introduced into legislation as the government recognised that corporate groups should be able to restructure without adverse tax consequences. However, this form of demerger has a number of strict conditions making it unsuitable for many business scenarios we encounter. For example, this demerger can only be used for trading companies not for investment companies, and cannot be used if there is an objective to sell part of the demerged group. Liquidation demergers have been widely used where a Statutory Demerger was not possible but involve the costs of liquidation.

The third form of demerger, the Capital Reduction Demerger, is now increasingly popular following changes to the Companies Act in 2008 that allow private company to reduce share capital with the support of a director’s statement of solvency, which is a fairly simple procedure. Previously a company would have required the consent of a court to reduce their share capital.

During a Capital Reduction Demerger part of the group (“the demerged assets”) are split out under a new company owned by all or some of the original shareholders. The mechanism used to achieve the demerger is a reduction of part of the share capital of the original group and cancellation of those shares. The share capital represented by those shares must be returned to the cancelled shareholders. This is fulfilled by transferring the demerged assets to a new company owned by those shareholders.

The demerger has the result that the demerged assets are now held by a separate new holding company, owned by some or all of the original shareholders of the original group. The retained assets of the original group remain within the original group. All original shareholders may remain with a smaller share capital or some shareholders are removed completely.

The usual tax reconstruction reliefs are used and advance clearance should be sought from HMRC disclosing all aspects of the transaction in detail. Detailed analysis of all the tax impacts is required to ensure unexpected tax charges do not arise and Entrepreneur’s Relief is maintained.

This form of demerger has a number of advantages over other forms of demerger including:

- No requirement for the entities to be trading companies;

- No legislative restriction on selling either part of the demerged group;

- No requirement for any company to be liquidated;

- The retained assets do not change ownership so reducing Stamp Duty or Stamp Duty Land Tax costs.

Capital Reduction Demergers can be a very useful and tax efficient method to split a corporate group. Our corporate finance team provide specialist advice to shareholders, management and companies on acquisitions, disposals and corporate restructurings. Please do not hesitate to contact us on 01491 579740.

Why HMT

Passionate

We are passionate about delivering an optimal outcome for our clients and helping them achieve their personal objectives. We understand entrepreneurial businesses because we are one

Our Deals

Personal

Partners are supported by high-calibre professional staff who share our core values of enthusiasm, energy, entrepreneurialism and empathy to our client’s objectives

Our Team

Proven

Our Partners have unparalleled deal experience in the mid-market and are supported by a team of dedicated deal-doers with specialist capabilities and experience

Our Awards

Connected

We have an extensive network of acquisitive corporates, institutional investors and debt providers both in the UK and internationally through our membership of our global network Cognos

Our NetworkLatest News