[White Paper] The UK’s Data Analytics Sector – M&A Activity & Value Drivers

The UK’s Data Analytics Sector : A Brief Overview

The UK’s data analytics market is best characterised as a high-growth, infrastructure-enabled sector. It’s a

market that combines strong enterprise demand, active public-sector programmes, as well as

infrastructure investment explicitly focused around AI and tech-heavy analytics. The UK’s data analytics

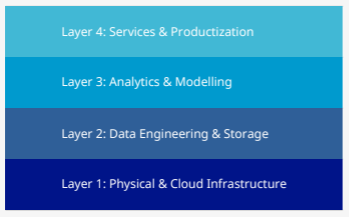

sector is multi-layered. At the foundation sit data infrastructure and cloud providers, such as UKCloud,

which supply storage, computing power and orchestration. Above this sit platforms for

data engineering, ETL (Extract, Transform, Load) and warehousing, analytics, BI tooling, specialised

machine-learning and ModelOps vendors. Sitting on top of this layer is a broad services layer made up of

strategy consultancies, system integrators and specialised analytics boutiques.

In 2025, commercial demand for

analytics is broad. Finance, retail,

healthcare and government remain the

largest spenders, while the supply side

is a layered mix. This year, several

structural forces define the market

including; robust revenue growth

expectations, a noticeable boom in

data-centre and hyperscale projects,

active public-sector programmes and a

regulatory environment that is

tightening around privacy and lawful

data use.

Market research in 2024-2025 points to double-digit growth trajectories and multi-billion-pound market

opportunity in the coming decade, with predictive and prescriptive analytics particularly prominent in

commercial forecasts. In 2024, the UK’s data analytics market had a revenue of £3,575 million, and with a

forecast CAGR of 25% over the next five years, the UK sector’s revenue could reach £13.3 billion by 2030.

Public-sector demand is currently a defining characteristic of the UK’s data analytics sector. National

health and government data strategies published in 2023 and 2024 have moved into implementation

phases across departments, resulting in an increase in spend on analytics capability and workforce

development. Similarly, rapid expansion of digital infrastructure, driven by the need to host generative-AI

has seen an acceleration in investment in UK data-centre capacity hyperscale projects. Across the market,

regulation and trust remain central constraints and differentiators.

Organisations are now under pressure to operate within UK GDPR and the Data Protection Act regime. For buyers and sellers in the current market, the ability to demonstrate robust governance, compliant data pipelines and ethical model design is as important as technical ability. In M&A terms, 2025 has been a year in which buyers have increasingly prioritised outcomes over toolkits. For example, recurring-revenue SaaS, outcome-based contracts and platform subscriptions are growing, but acquirers require proof of ROI and operational embedding. Overall, the landscape of the UK’s data analytics market is one of significant addressable demand, accelerating infrastructure and supportive public-sector programmes.

On the other hand, the sector indicates persistent skills gaps, regulatory complexity and intense global

competition.

Trends and Shifts in the UK’s Data Analytics Market

Until now, the UK’s data analytics market has acted as a supporting function for reporting and insight. In

2025, it has become a core operational and competitive necessity. Organisations across finance,

healthcare, retail and government are now designing around data, rather than simply analysing it.

Analytics budgets are increasingly tied to measurable outcomes such as productivity, risk reduction and

customer personalisation, rather than (as previously) more experimental proof-of-concept projects. As a

result, there has been a major shift away from focus on potential towards performance, meaning firms

within the sector are now under pressure to demonstrate tangible returns from their data estates.

One of the primary trends underpinning this recent transformation is the rise of AI-enabled analytics.

According to UK Government research, the UK’s AI market was worth more than £72 billion in 2024, with

around 16% of all UK organisations adopting at least one AI technology. These statistics reflect the

widespread integration of machine learning and generative AI into analytic workflows, allowing

businesses to automate data preparation, improve predictive accuracy and support decision-making at

scale. Instead of replacing analysts, these tools augment human expertise, allowing teams to model

complex systems and forecast with greater precision. However, this trend has resulted in new governance

demands such as model monitoring and bias mitigation, especially in regulated industries such as finance

and healthcare.

Another defining trend in the UK’s data analytics market, is the expansion of data infrastructure capacity,

driven by a growing network of hyperscale data centres and cloud regions across the UK. Large-scale

investments, such as YFM’s £8.5 million investment into Plandek, have reshaped the analytics ecosystem,

reducing data transfer delays, enabling heavier computational loads and attracting foreign investment.

This growth is not just technical, it signals the UK’s strategic positioning in the global data economy. With

major projects emerging across London, Manchester and Scotland’s central belt, growing analytics

workloads can be run domestically at scale. The public sector and healthcare remain central to the data

analytics landscape in the UK. The NHS’s ongoing digital transformation has accelerated the adoption of

data-driven planning, population analytics and predictive modelling. Government departments have also

begun expanding their data-sharing networks to enable service optimisation. However, this expansion

has put a spotlight on privacy and data ethics. In 2025, sellers and public bodies are expected to not only

comply with regulation, but to demonstrate trustworthiness as a source of competitive and reputational

advantage. This has resulted in organisations all over the country opting to prioritise compliance with

regulations such as the General Data Protection Regulation (GDPR). In order to maximise the use of data

for strategic insights, UK businesses are also increasingly investing in secure data management practices,

ensuring they meet legal requirements.

Despite being mainly tech-focused, talent and capability continue to shape the trajectory of the UK’s data

analytics sector. Demand for senior data engineers, cloud architects and applied data scientists continues

to outweigh supply. The market has been quick to respond, implementing in-house academies and

apprenticeship programmes aimed at closing the skills gap. For example, organisations such as BT Group

and NatWest have launched apprenticeship schemes specifically targeting data roles. However, there are

still notable shortages in senior and specialised roles including data engineers, who can design scalable

pipelines, cloud architects capable of managing hybrid analytics environments and applied data scientists

skilled in operationalising models within regulated industries. The most effective analytics professionals

are those who combine computational skill with storytelling, stakeholder management and strategic

thinking. As a result, this combination of technical precision and business acumen has become a key

differentiator in the market.

[…]

Drivers of M&A in the UK’s Data Analytics Sector

Throughout 2024 and 2025, M&A activity within the UK’s data analytics market has accelerated

significantly, reflecting the sector’s increasingly central role in the digital economy. The dynamics of the

market, including a combination of high growth potential, fragmented supplier ecosystems and global

competition, have made consolidation a strategic necessity for many firms. The recent surge in M&A

activity is being driven by a mixture of technological imperatives, investor appetite and the race to secure

talent and capability.

One of the foremost drivers of M&A in the sector is capability convergence. As the term “analytics”

becomes increasingly inseparable from AI, cloud computing and digital infrastructure, firms are seeking

to broaden their service portfolios through acquisition, as opposed to organic growth. Traditional

business intelligence providers have started to acquire machine learning specialists, as AI start-ups are

being absorbed by larger consultancies and cloud infrastructure firms are integrating analytics

capabilities to offer end-to-end data solutions. Clients are increasingly demanding holistic data strategies

that move seamlessly from architecture and storage, to modelling, insight delivery and operational

integration. Acquiring these capabilities enables firms to accelerate time-to-market and enhance

credibility in competitive tenders. An equally powerful driver is the pursuit of scale and market reach. The

UK’s analytics ecosystem remains highly fragmented, with hundreds of small and mid-sized firms offering

services that overlap. Consolidation allows acquirers to integrate customer bases, expand geographical

reach and gain the operational resilience required to compete for larger, multi-year contracts. This is

particularly popular in the public sector, where procurement frameworks increasingly favour businesses

with demonstrated scale, security credentials and delivery history.

International buyers, especially from the US and Europe, continue to view the UK as a gateway into EMEA

markets. This is due to the UK’s deep talent pool, regulatory clarity and proximity to major financial

centres. As a result, inbound M&A remains a defining feature of the UK’s data analytics landscape, with

firms frequently serving as regional platforms for global expansion. Talent acquisition is another key

driver for deal activity in the sector. The shortage of experienced data engineers, cloud architects and

applied data scientists has resulted in skilled teams becoming a premium asset in their own right. For

many acquirers, purchasing a smaller analytics consultancy is faster and more effective than attempting

to recruit, or train, equivalent expertise. Such deals not only secure immediate capability, they also bring

an entrepreneurial culture and agile delivery models into larger businesses. The increased competition for

talent has blurred the line between strategic and defensive acquisitions. Firms are now buying to grow, as

well as to prevent competitors from accessing the same talent. […]

If you want to receive a copy of the full white paper, please email Melissa Dainelli at [email protected].

Why HMT

Passionate

We are passionate about delivering an optimal outcome for our clients and helping them achieve their personal objectives. We understand entrepreneurial businesses because we are one

Our Deals

Personal

Partners are supported by high-calibre professional staff who share our core values of enthusiasm, energy, entrepreneurialism and empathy to our client’s objectives

Our Team

Proven

Our Partners have unparalleled deal experience in the mid-market and are supported by a team of dedicated deal-doers with specialist capabilities and experience

Our Awards

Connected

We have an extensive network of acquisitive corporates, institutional investors and debt providers both in the UK and internationally through our membership of our global network Cognos

Our NetworkLatest News