Throughout 2020 and 2021, an acceleration in e-commerce and pressure on global supply chains, principally brought about by the pandemic, drove updemand for transport and logistic services and, therefore, freight prices. M&A activity followed suit as sellers were enticed by growing valuation multiples, and buyers were drawn to the sector because of the significant changes occurring, the magnitude of which could potentially reinvent the sector.

However, in the latter half of 2022, the tightening of pricing on last mile delivery, the stabilisation of supply chains, increased energy / fuel costs brought about the Ukraine conflict, ongoing tightening of the labour market and an increased capital cost have cooled the red-hot deal activity of the past 24 months.

Going into 2023, the e-commerce market continues to swell, with contemporary consumer trends, which have accelerated during the pandemic, and modern consumption habits indicating pure-play online retailing is likely to continue to grow. Accordingly, cost-conscious businesses and the e-commerce market are expected to be avenues for sustained growth in logistics outsourcing. According to Insider Intelligence, e-commerce sales are forecast to grow annually by approximately 4.2% between 2022 and 2026, outpacing non-e-commerce which is forecast to grow annually by 2%, evidencing the growth opportunities for 3PL providers in the e-commerce market. This combined with an ongoing propensity for SME retailers to outsource 3PL services to manage committed operating costs continues to provide growth for the market.

Key Sector M&A drivers in 2023

Market consolidation

Whilst overall M&A activity cooled in 2022, the industry was dominated by consolidation in what remains a fragmented market. The largest transaction in the sector in 2022 saw Clipper Logistics acquired by GXO (formerly a fulfilment division of XPO which was carved out and separately listed in 2021), who sought to consolidate their position in the UK market.

In the mid-market, the consolidation trend we’ve seen over the past ten years is set to continue, fuelled by a significant level of buy and build activity from PE backed businesses. With institutions needing to deploy significant levels of dry powder, and with exceptionally strong balance sheets across both large international logistics companies and mid-market operators, many remain keen to acquire businesses in growing areas of the industry.

With the industry seemingly destined to become dominated by fewer, bigger businesses; SME market participants lacking operational scale may struggle more with challenging economic conditions and suffer a reduced ability to compete. This may be compounded by the need to invest in new low-carbon delivery methods and other sustainability-focused technology in order to satisfy their customers’ growing ESG requirements. As companies consolidate, merge, and invest, smaller businesses will need to stay competitive by enhancingtheir service proposition to clients to thrive.

For many of the more established mid-market operators, the cash generated during the strong pandemic years has been re-invested into state-of-the-art facilities and there is now a push to increase utilisation by acquiring smaller, less efficient businesses to consolidate into these new premises, which will enable them to generate quick synergies.

Vertical integration

Traditional retailers, not just logistics companies, have made a big splash in the M&A market, causing heightened acquirer demand, and pushing valuations higher. In the US for example, Quiet Logistics, a rapidly growing third-party logistics provider with a focus on e-commerce, was acquired by American Eagle Outfitters in December 2021 for a total enterprise value of $360 million. Quiet Logistics will join American Eagle as their second logistics acquisition of 2021, followingr its acquisition of AirTerra in August 2021. What happens in the US tends to be a pre-cursor for M&A activity in the UK, and in September 2022 Marks & Spencer Group plc acquired Gist Ltd, the local supply chain specialist and solutions provider, from Linde plc for £255 million.

These acquisitions demonstrate how retailers are leveraging logistics as a strategic tool where scale allows, bringing fulfilment back in-house to reduce costs and generate efficiencies within their own businesses. Many are retaining third party customers within these sites to benefit from the operational scale of the acquired business and creating a positive contribution to what would historically have been a cost centre.

Inbound Investment

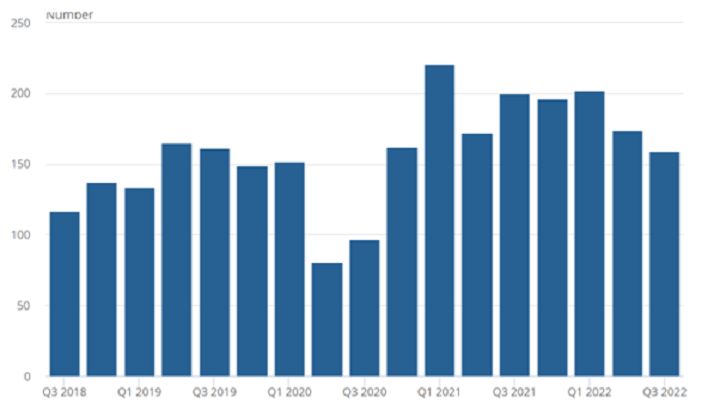

Overall, the number of acquisitions in UK companies from overseas investors increased above pre-pandemic levels in 2022 – this was fuelled by a weakening of the pound, albeit after Q2 2022. cross-border activity slowed due to geopolitical uncertainty following Russia’s invasion of Ukraine.

The number of inward M&A between Quarter 3 2018 and Quarter 3 2022

Source: Office for National Statistics – Mergers and Acquisitions Survey

In 2023 UK logistics businesses will remain attractive as a gateway into Europe. However industry operators using old technology and legacy systems are considered less reliable and may not be in a position to provide clients with the information necessary to ensure a seamless flow of goods to and from the European Union. Proactive 3PL providers that have invested in next generation logistics technologies, such as WMS systems, order fulfilment software applications and other cloud-based platforms; and those that are knowledgeable of changes to post Brexit customs procedures are likely to be more attractive to acquirers and investors as they will be able to demonstrate the ability to retain those clients seeking to outsource their international supply chain management.

Conclusion

The UK 3PL market remains highly fragmented and is made up of approximately 14,900 active providers, of which the majority are small to medium-size firms focusing on local business and supply-chain-function specific markets. As a result, there will undoubtedly continue to be a significant level of consolidation in the sector.

Notwithstanding this, the concerns slowing M&A at the end of 2022 will linger and are likely to result in both a hardening of prices and / or deals structured with an element of earn-out in those circumstances where sellers remain bullish about the prospects of growth and expect to be fully compensated for it.

For over 30 years, HMT has advised hundreds of ambitious entrepreneurial businesses, helping them to build and realise value. Our recent sector experience has given us access to numerous trade acquirers and institutional investors seeking acquisitions in the sector, and we would welcome the opportunity to have an initial conversation to share some of the insights we have as well as to understand the ambitions of any shareholders or management teams contemplating a transaction.

Throughout 2020 and 2021, an acceleration in e-commerce and pressure on global supply chains, principally brought about by the pandemic, drove updemand for transport and logistic services and, therefore, freight prices. M&A activity followed suit as sellers were enticed by growing valuation multiples, and buyers were drawn to the sector because of the significant changes occurring, the magnitude of which could potentially reinvent the sector.

However, in the latter half of 2022, the tightening of pricing on last mile delivery, the stabilisation of supply chains, increased energy / fuel costs brought about the Ukraine conflict, ongoing tightening of the labour market and an increased capital cost have cooled the red-hot deal activity of the past 24 months.

Going into 2023, the e-commerce market continues to swell, with contemporary consumer trends, which have accelerated during the pandemic, and modern consumption habits indicating pure-play online retailing is likely to continue to grow. Accordingly, cost-conscious businesses and the e-commerce market are expected to be avenues for sustained growth in logistics outsourcing. According to Insider Intelligence, e-commerce sales are forecast to grow annually by approximately 4.2% between 2022 and 2026, outpacing non-e-commerce which is forecast to grow annually by 2%, evidencing the growth opportunities for 3PL providers in the e-commerce market. This combined with an ongoing propensity for SME retailers to outsource 3PL services to manage committed operating costs continues to provide growth for the market.

Key Sector M&A drivers in 2023

Market consolidation

Whilst overall M&A activity cooled in 2022, the industry was dominated by consolidation in what remains a fragmented market. The largest transaction in the sector in 2022 saw Clipper Logistics acquired by GXO (formerly a fulfilment division of XPO which was carved out and separately listed in 2021), who sought to consolidate their position in the UK market.

In the mid-market, the consolidation trend we’ve seen over the past ten years is set to continue, fuelled by a significant level of buy and build activity from PE backed businesses. With institutions needing to deploy significant levels of dry powder, and with exceptionally strong balance sheets across both large international logistics companies and mid-market operators, many remain keen to acquire businesses in growing areas of the industry.

With the industry seemingly destined to become dominated by fewer, bigger businesses; SME market participants lacking operational scale may struggle more with challenging economic conditions and suffer a reduced ability to compete. This may be compounded by the need to invest in new low-carbon delivery methods and other sustainability-focused technology in order to satisfy their customers’ growing ESG requirements. As companies consolidate, merge, and invest, smaller businesses will need to stay competitive by enhancingtheir service proposition to clients to thrive.

For many of the more established mid-market operators, the cash generated during the strong pandemic years has been re-invested into state-of-the-art facilities and there is now a push to increase utilisation by acquiring smaller, less efficient businesses to consolidate into these new premises, which will enable them to generate quick synergies.

Vertical integration

Traditional retailers, not just logistics companies, have made a big splash in the M&A market, causing heightened acquirer demand, and pushing valuations higher. In the US for example, Quiet Logistics, a rapidly growing third-party logistics provider with a focus on e-commerce, was acquired by American Eagle Outfitters in December 2021 for a total enterprise value of $360 million. Quiet Logistics will join American Eagle as their second logistics acquisition of 2021, followingr its acquisition of AirTerra in August 2021. What happens in the US tends to be a pre-cursor for M&A activity in the UK, and in September 2022 Marks & Spencer Group plc acquired Gist Ltd, the local supply chain specialist and solutions provider, from Linde plc for £255 million.

These acquisitions demonstrate how retailers are leveraging logistics as a strategic tool where scale allows, bringing fulfilment back in-house to reduce costs and generate efficiencies within their own businesses. Many are retaining third party customers within these sites to benefit from the operational scale of the acquired business and creating a positive contribution to what would historically have been a cost centre.

Inbound Investment

Overall, the number of acquisitions in UK companies from overseas investors increased above pre-pandemic levels in 2022 – this was fuelled by a weakening of the pound, albeit after Q2 2022. cross-border activity slowed due to geopolitical uncertainty following Russia’s invasion of Ukraine.

The number of inward M&A between Quarter 3 2018 and Quarter 3 2022

Source: Office for National Statistics – Mergers and Acquisitions Survey

In 2023 UK logistics businesses will remain attractive as a gateway into Europe. However industry operators using old technology and legacy systems are considered less reliable and may not be in a position to provide clients with the information necessary to ensure a seamless flow of goods to and from the European Union. Proactive 3PL providers that have invested in next generation logistics technologies, such as WMS systems, order fulfilment software applications and other cloud-based platforms; and those that are knowledgeable of changes to post Brexit customs procedures are likely to be more attractive to acquirers and investors as they will be able to demonstrate the ability to retain those clients seeking to outsource their international supply chain management.

Conclusion

The UK 3PL market remains highly fragmented and is made up of approximately 14,900 active providers, of which the majority are small to medium-size firms focusing on local business and supply-chain-function specific markets. As a result, there will undoubtedly continue to be a significant level of consolidation in the sector.

Notwithstanding this, the concerns slowing M&A at the end of 2022 will linger and are likely to result in both a hardening of prices and / or deals structured with an element of earn-out in those circumstances where sellers remain bullish about the prospects of growth and expect to be fully compensated for it.

For over 30 years, HMT has advised hundreds of ambitious entrepreneurial businesses, helping them to build and realise value. Our recent sector experience has given us access to numerous trade acquirers and institutional investors seeking acquisitions in the sector, and we would welcome the opportunity to have an initial conversation to share some of the insights we have as well as to understand the ambitions of any shareholders or management teams contemplating a transaction.